PRESENCE OF LONG MEMORY 1

by

Walter Kramer and Philipp Sibbertsen

Fachbereich Statistik,Universitat Dortmund, D-44221Dortmund, Germany

VersionJune 2000

Abstract

Wederivethe limitingnulldistributionsofthe standardandOLS{

based CUSUM-tests for structural change of the coecients of a

linearregressionmodelinthecontextoflongmemorydisturbances.

We show that both tests behave fundamentallydierent ina long

memoryenvironment,ascomparedtoshortmemory,andthatlong

memory is easily mistaken for structural change when standard

critical values are employed.

1 Introduction and Summary

It is by now well known that long memory and structural change are easily

confused(Lobatoand Sawin1997,Engleand Smith1999,Grangerand Hyung

1999, Diebold and Inoue 1999 and many others). Therefore it is of interest

to know about both the stochastic properties of procedures for detecting and

measuring long memory when there isonly structural change,and ofthe per-

formance of tests for structural change when there isonly long memory.

1

ResearchsupportedbyDeutscheForschungsgemeinschaft;weare gratefulto A. Zeileis

forexpert computationalassistance.

been rather little work on the latter (Hidalgo and Robinson 1996, Wright

1998). Below we consider the behaviour of the standard and the OLS-based

CUSUM-tests,whose limitingdistributionsare wellunderstoodinthe context

of variousregressor-sequences and iid-orshort memorydisturbances(Kramer

et al. 1988, Ploberger and Kramer 1992, 1996). As shown by Wright (1998)

for theOLS-based CUSUM-test andthe special caseof polynomialregressors,

these limiting distributions are not robust to departures from short memory

- in fact, the OLS-based CUSUM-test has an asymptotic size of unity. The

present paperallows for more generalregressor sequences alsocovers the con-

ventional CUSUM-test based on recursive residuals as well. We show that

Wright's results concerning the behaviour under H

0

essentially go through

with more general regressors, and that similar results hold for the standard

CUSUM-test. This is a rather negative result which conrms related theo-

rems fromthe structural-change-mistaken-for-long-memory-literature:Similar

tostructural changebeingmistaken forlong memory,longmemory islikewise

easily mistaken for structural change, and it is remains an open problem to

eciently discriminate between the two 2

.

2 Two unpleasant theorems

Weconsider the standard linear regression model

y

t

= 0

x

t +"

t

; (t=1;:::;T) (1)

with nonstochastic, xed regressors x

t

and stationary mean zero disturbances

"

t

. We assumethat

1

T T

X

t=1 x

t

! c<1 and (2)

2

There do exist solutionsfor somespecial cases,such asKunsch's (1986)procedure to

discriminate betweenlongmemory and monotonictrends, but ageneral treatment ofthis

problemisstillmissing.

1

T X

t=1 x

t x

0

t

! Q(nite, nonsingular): (3)

Theseare standardassumptions inlinearregression largesampleasymptotics;

theyexcludetrendingdata,whichrequireseparatetreatmentandproofswhich

dier fromthe ones below.

Weare concerned withtesting the model(1) againstthe alternativeof unspe-

cied structural change in the regression coecients . We consider rst the

OLS{based CUSUM{test, asproposed by Ploberger and Kramer (1992).This

test rejects the nullhypothesis of nostructural changefor large values of

TS := sup

0<<1 jC

T

()j; where (4)

C

T

() := T 1

2

^

1

"

[T]

X

t=1 e

t

; (5)

and where e

t :=y

t x

0

t

^

are the OLS{residuals from(1).

The limiting null distribution of TS is well known for white noise and short

memory disturbances. Our rst theorem extends these results to stationary

long memory disturbances, where the "

t

followa stationaryARFIMA(p,d,q){

process:

E("

t

"

t k

)=L(k)k d

; (6)

L(k)slowlyvarying, 0<d<1=2.

Theorem 1 In the regression model (1), with disturbances as in (6) we have

T d

C

T

()!B

d

() c 0

Q 1

(); (7)

where B

d

() is fractional Brownian Motion with self-similarity parameter d

and ()N(0;

2

"

Q).

C

T

() = T 1

2

^

1

"

8

<

: [T]

X

t=1

"

t [T]

X

t=1 x

0

t T

X

t=1 x

t x

0

t

!

1

T

X

t=1 x

t

"

t 9

=

;

; so (8)

T d

C

T

() = (

T d+

1

2

z

[T]

T d+

1

2 [T]

X

t=1 x

0

t T

X

1 x

t x

0

t

!

1

T

X

1 x

t

"

t )

=^

"

; (9)

where z

t

=z

t 1 +"

t , z

0

=0.In viewof

T d

1

2

z

[T]

!

"

B() (see e.g. Marmol 1995); (10)

1

T [T]

X

t=1 x

t

! c; (11)

0

@ 1

T [T]

X

t=1 x

t x

0

t 1

A 1

!

1

Q 1

; (12)

T d

1

2 [T]

X

t=1 x

t

"

t

! () (see Giraitisand Taqqu 1998); (13)

and

^ 2

"

= T

X

t=1 e

2

t

T

= T

X

t=1

"

2

T +o

P

(1)! 2

"

the limiting relationship(7) follows. 2

>From (7), it is immediately seen that TS P

! 1 under H

0

, so the OLS-

based CUSUM{test is extremely non{robust to long{memory disturbances,

in the sense that long memory is easily mistaken for structural change when

conventional criticalvaluesare employed.

Next we consider the standard CUSUM-test based onrecursiveresiduals

~ e

t

= y

t x

0

t

^

(t 1)

f

t

;

^

(t 1)

=

X (t 1)

0

X (t 1)

1

X (t 1)

0

y (t 1)

(14)

f

t

=

1+x 0

t (X

(t 1) 0

X (t 1)

) 1

x

t 1

2

(t=K+1;:::;T); (15)

It rejects for large valuesof

S

T

= sup

0<<1 W

T

()=(1+2): (16)

where

W

T

():=T 1

2

^

1

"

[T]

X

t=K+1

~ e

t

: (17)

Theorem 2 In the regression model (1), with disturbances as in (6) we have

T d

W

T

()!B

d

(); (18)

whereagainB

d

()isfractionalBrownianMotionwithself-similarityparameter

d.

PROOF:Following Kramer et al.(1988), wewrite W

T () as

W

T ()=

1

p

T [T]

X

t=K+1

"

t

[T]

X

t=K+1

^

(t 1)

0

x

t

: (19)

Let Q

j :=

1

T P

j

i=1 x

i x

0

i

.First we showthat

max

KtT jj

^

(t)

t

X

j=K [(y

j x

0

j )x

j ]Q

1

j

jj=o

p

T d+

1

2

(ln ln T) 1

2

:(20)

LetS

t :=

P

t

j=1 (y

j x

0

j )x

j

.Bythe lawofthe iteratedlogarithmforthe sums

of long memory Gaussian random variables we have for some slowly varying

function L(T)

max

1tT

S

t

2

(d+

1

2 )2(d+

1

2 ) 1

T 2(d+

1

2 )

L(T) ln ln(T) 1

2

=O

p

(1); (21)

so (20) follows directlyfrom Lemma3.1 of Jureckova and Sen (1984).

1

p

T [T]

X

t=K+1 (y

t x

0

t

^

(t 1)

)

= 1

p

T [T]

X

t=1 t

X

j=1 c

ij (y

j x

0

j

)+o(T (d+

1

2 )

ln ln T) 1

2

; (22)

where

c

ij

= 8

>

>

>

<

>

>

>

: x

0

j Q

1

(i 1) x

i

i>j

1 i=j

0 i<j

(23)

(see also Sibbertsen, 2000). In viewof a result by Sen (1984) that

X

ji c

2

ij

=1+0(

1

i

) (24)

and theorem 5.1of Taqqu (1975),the theorem now follows from (22). 2

Theorem2showsthatthenulldistributionofthestandard CUSUM-testtends

toinnityaswell,sothestandardCUSUM-testhaslikewiseanasymptoticsize

of unity.

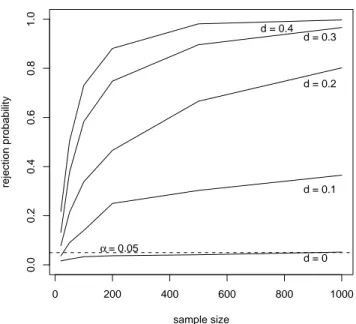

3 Some nite sample Monte Carlo evidence

Figure1belowgivestheempiricalrejectionrates,using1000runsandstandard

critical values form the iid-disturbance case, for the OLS-based CUSUM-test.

WhenthedisturbancesareinfactARFIMA(0,d,0).Itconrmesourtheoretical

results:rejectionratesincreasewithdandsamplesize,andproducemisleading

evidence even for smalld and T.

0 200 400 600 800 1000

0.00.20.40.60.81.0

sample size

rejection probability

α= 0.05

d = 0 d = 0.1 d = 0.2 d = 0.3 d = 0.4

Figure 1:Empiricalrejection probabilityof OLS-basedCUSUM-test

0 200 400 600 800 1000

0.00.20.40.60.81.0

sample size

rejection probability

α= 0.05

d = 0 d = 0.1 d = 0.2 d = 0.3 d = 0.4

Figure2:Empiricalrejection probabilityofstandard CUSUM-test

Figure 2 gives the corresponding empirical rejection rates for the standard

CUSUM-test. Notsurprisingly,the empiricalsize isnot as far othe mark as

for the OLS-based CUSUM-test, but the test is misleadinghere as well.

Diebold, F.S. and Inoue, A. (1999): "Long memory and structural

change." Stern Schoolof Business discussion paper.

Engle, R.F. and Smith, A. (1999): "Stochastic permanent breaks." Re-

view of Economics and Statistics

Giraitis, L. and Taqqu, M. (1998): "Convergence of normalized quadra-

tic forms." To appear in Journal of Statistical Planning and Inference

80,15 {35.

Granger, C.W.J. and Hyung, N. (1999): "Occasional structural breaks

and long memory."UCSD discussion paper 99-114.

Hidalgo, J. and Robinson, P.M. (1996): "Testing for structural change

inalong{memoryenvironment."Journal of Econometrics70,159{174.

Jureckova, J. and Sen, P.K. (1984): "On adaptive scale-equivariant M-

estimators in linearmodels."Statistics and Decision 2, 31{ 46.

Kunsch, H. (1986): "Discrimination between monotonic trends and long

range dapendence." Journal of Applied Probability23,1025 { 1030.

Kramer, W.; Ploberger, W. and Alt, R. (1988): "Testing for structu-

ralchangein dynamic models."Econometrica56, 1355 {1369.

Lobato, I.N. and Savin, N.E. (1997): "Real and spurious lon-memory

properties of stock market data (with discussion and reply)." Journal

of Business and Economic Statistics 16,261 {283.

Marmol, F. (1995): "Spurious regression between I(d){processes."Journal

of Time Seies Analysis16,313 {321.

Ploberger, W. and Kramer, W. (1992): "The CUSUM{test with OLS{

residuals." Econometrica 60,271 { 286.

Ploberger, W. and Kramer, W. (1996): "A trend{resistent test for

structuralchange basedonOLS{residuals."Journal of Econometrics70,

175 { 185.

Sibbertsen, Ph. (2000): "Robust CUSUM-M-test in the presence of long

memory disturbances." TechnicalReport 19/2000,SFB 475, Universitat

Dortmund.

Taqqu, M.S. (1975): "Weak convergence of fractionalBrownian Motion to

the Rosenblatt process." Zeitschrift fur Wahrscheinlichkeitstheorie und

verwandte Gebiete 31,287 {302.

long-memory disturbances." Journal of Time Series Analysis 19, 369 {

379.