Bayesian Inference for High-Dimensional Data with Applications to Portfolio Theory

150

0

0

Volltext

(2)(3)(4)(5)

(6)(7)

(8)(9)

(10)(11)

(12)(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

(21)

(22)

(23)

(24)

(25)

(26)

(27)

(28)

(29)

(30)(31)

(32)

(33)

(34)

(35)

(36)

(37)

(38)

(39)

Abbildung

+7

ÄHNLICHE DOKUMENTE

Inwiefern sind E-Portfolios ein geeignetes Instrument, um selbstgesteuerte Lernprozesse zu unterstützen?...

It will be shown that the mean-variance hedging problem in nance of this context is a special case of the linear quadratic optimal stochastic control problem discussed in Section 5,

We measure the (annualized) average ΔMPPM over a random hedge fund portfolio as the MPPM of the alternative asset strategy (90% invested into the original pension fund and 10%

I drilled holes for the screw connected to the holder. Unfortunately the screws did not fit after my first try, and I had to re-drill the holes. The next time, I will check the size

In the aftermath of any agreement, the United States (and the international community) must also maintain the will and capability to take effec- tive action, including the use

Keywords: Catastrophes, Insurance, Risk, Stochastic optimization, Adaptive Monte Carlo, Nonsmooth optimization, Ruin probability.... 3 2.3 Pareto

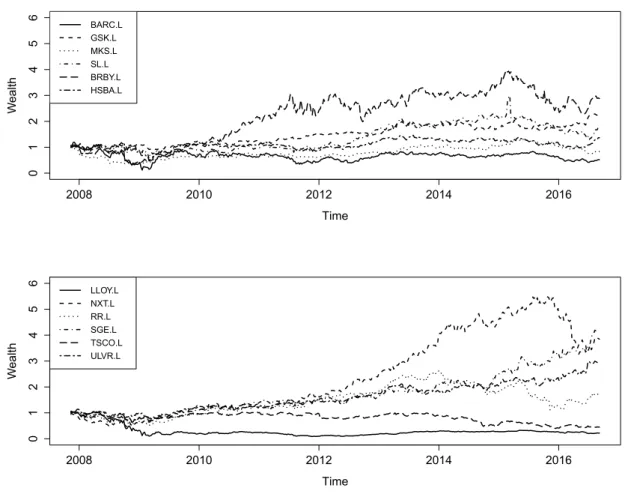

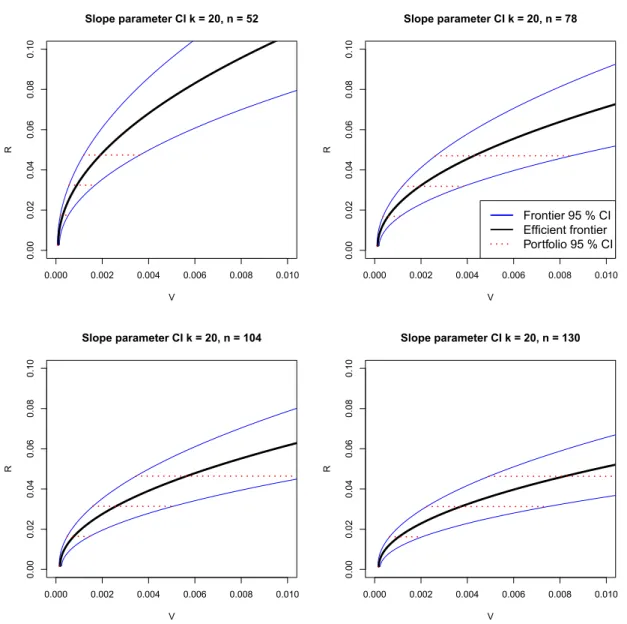

In this section, we discuss the procedure of a typical Bayesian portfolio selection. On the basis of her forecast of future stock returns, she optimally allocates the

Based on the normality assumption and on ¯ r and S as plug-in estimates, the distri-.. This will cause large short positions in the constructed portfolio. In the following, we